Big Media Growth Playbook

We Know the Bear Case, What Could Go Right?

In the grand tradition of windowing in media, starting December 2023, all my writing will be posted first on my Substack, The Mediator, and posted on Medium one week later.

Sign up for free to get The Mediator delivered to your inbox “day-and-date”!

The woes of the big media companies (Disney, Fox, NBC Universal, Paramount and WarnerBros. Discovery) have been well documented: linear TV is in decline; streaming has not proved the panacea most hoped; the box office is weak, with many prospective blockbusters disappointing of late; the ad environment is tepid; and two strikes are underway, both the WGA and SAG-AFTRA, with little sign they’ll be resolved soon. And while generative AI isn’t affecting the business yet, in recent weeks the threat it poses has come center stage (something I’ve written about a lot over the last six months, such as here, here, here and here).

Investors are bearish, the press is brutal and morale in Hollywood is turning ever darker. We know the bear case, but what could go right?

Put differently, can big media grow and, if so, how?

Tl;dr:

- Some of the conglomerates are clearly positioned better than others, but the reality is that, in general, it will be very challenging to grow. The media conglomerates are essentially video companies (>80% of revenue); most of this is linear (~60%), which is declining; the overall video business is already massive (in terms of time and money); and video arguably over-monetizes relative to other forms of media.

- For perspective, a 1% annual decline in the U.S. “video business” (linear, streaming and studio) over 5 years would produce a $10 billion hole that needs to be made up somewhere else.

- But the conglomerates have a few things going for them. Some of their problems are self-inflicted and can therefore be reversed; people spend an enormous amount of time watching video; they make a product people love; they own or control vast amounts of IP; and while Internet economics are always value destructive for incumbents, they can try to exploit lower costs.

- This yields a framework for thinking through potential sources of growth. They can “fix it” (reverse some of the destructive decisions make in the rush to streaming, a process that is already underway); better monetize attention; better monetize engagement; capitalize on Internet economics; or shrink-to-grow.

- Below, I provide an overview of specific opportunities in each category. Fix it (operational optimization, industry structure rationalization and “verticalization” of video offerings); better monetize attention (addressable/programmatic advertising and shoppable TV); better monetize engagement (gaming/metaverse, XR, NFTs and fan creation); exploit Internet economics (international streaming and lower cost production technologies); and shrink-to-grow.

- Several things jump out from this exercise. There are no easy answers and no silver bullets. Many of these opportunities are highly speculative and/or will take a long time. Some entail more risk than the conglomerates are probably willing to take. But, in totality, they could help.

- The industry is reeling from a one-two punch over the last 18 months. Linear declines are accelerating and the big bet on streaming isn’t paying off. It’s understandable why the conglomerates have focused foremost on retrenching. But clawing their way back to profitability in streaming and making good content is not a long-term growth strategy. At some point they need to answer the following question: What now?

Disclaimer: Note that the opinions expressed here do not necessarily reflect those of Boston Consulting Group.

Why Growth Matters

The importance of growth is so ingrained in our thinking that we don’t often ask: do companies really need to grow?

In theory, they don’t. A stagnant, or even declining, business that generates a lot of free cash flow could be a great investment (depending on the valuation at which you bought it and how the cash flow is deployed). In practice, however, it is very challenging for a public company to concede lack of growth for a few reasons.

- It’s a tough story to tell both externally and internally without making it sound like the company has given up. Lack of growth is equated with lack of imagination and initiative.

- It damages morale and makes it hard to attract and retain talent. Employees want to work for a company that is winning and no-growth is synonymous with losing.

- Even if a company comes out and says it — “it was good while it lasted, but we won’t be growing from here” — there will still be pressure from investors to manufacture growth (such as through more aggressive cost cutting) and vulnerability to hostile acquirers or activists who think they can do better.

- Plus, it’s hard to justify high levels of executive compensation if you’re shepherding a business into its decline.

So, companies facing structural growth challenges are under tremendous pressure to figure a way out.

The Problem: Video Is Big

I try to be a pragmatic optimist: being both realistic about the challenges and hopeful about the future. In that spirit, let’s first confront the challenges to growth.

Media Conglomerates are Video Companies

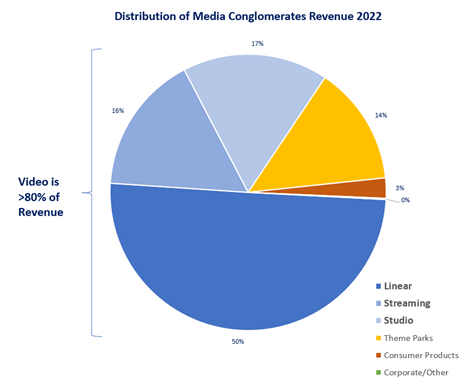

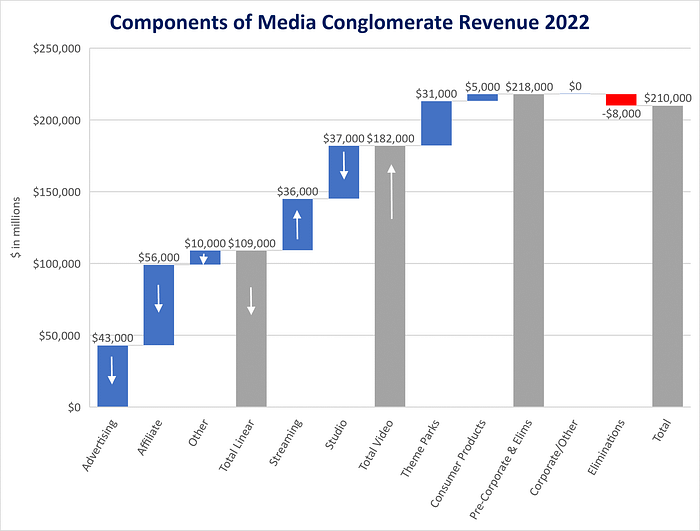

“Media conglomerates” — by which I mean Disney, Fox, NBCUniversal (a division of Comcast), Paramount and WarnerBros. Discovery — is a misnomer. Usually, the word “media” comprises print (newspapers, magazines, books, online publishers), audio (radio, streaming audio, podcast), video (linear TV, streaming, home video, box office), gaming and even social media. These businesses are heterogenous, of course (most notably, both Disney and NBC Universal have significant theme park operations and Disney has a much larger consumer products business) but, in totality these companies are really video companies (Figure 1).

In 2022, more than 80% of their global revenue was derived from video-related activities, including linear networks, streaming and their studio businesses. Linear was roughly half of all revenue and 60% of video revenue. Note also that much of the Studio revenue line is tied to linear network customers, whether intercompany or third party broadcast and cable networks.

More than 80% of “media conglomerates” revenue is derived from video and linear video (broadcast and cable networks) represents 60% of that

Figure 1. Media Conglomerates are Really Video Conglomerates

Note: Reflects aggregate revenue for Disney, Fox, NBCUniversal, Paramount and WarnerBros. Discovery for fiscal 2022, before intercompany eliminations. Does not adjust for non-calendar fiscal years (Disney is September, Fox is June). Only Disney breaks out Consumer Products, so small amounts of consumer products revenue are embedded in other categories, but amounts are insignificant. Theme Parks represents both Disney and NBCU theme parks. Source: Company reports, author estimates

Video is No Longer Growing

So, most of the conglomerates’ revenue is video and most of the video revenue is linear. And linear is in decline. I won’t belabor the point, because the dynamics here are well understood, but I’ll post two graphs to show why.

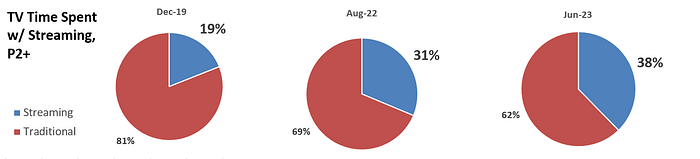

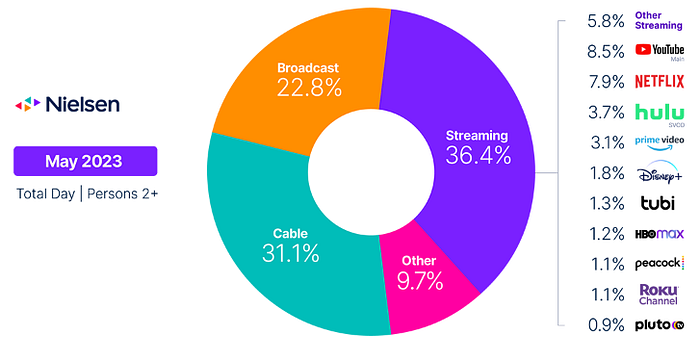

Linear revenue comprises both advertising sales and affiliate fees. As shown in Figure 2, linear viewership is rapidly losing share to streaming and, since overall TV viewing is relatively stagnant, that means that absolute viewership levels are steadily falling. While broadcasters and cable programmers have been generally able to eke out some pricing for their ad inventory, it hasn’t been enough to offset the viewership declines, so advertising revenue is falling.

Figure 2. Linear Viewing is Rapidly Losing Share to Streaming

Source: Nielsen

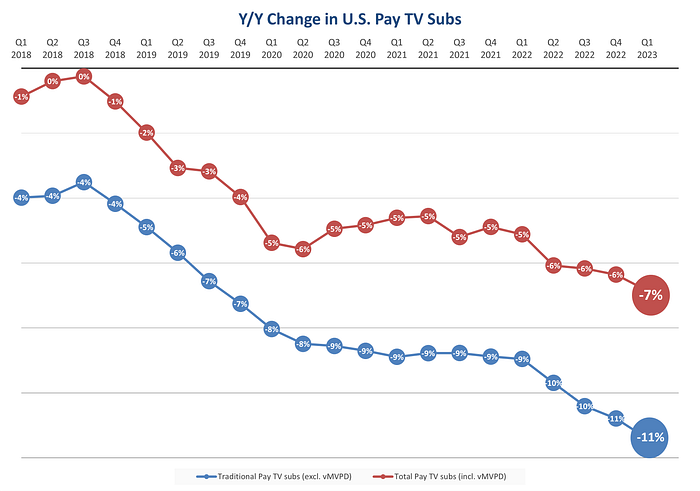

At the same time, the rate of pay TV subscriber declines has also been accelerating recently (Figure 3). While affiliate fee price increases had been enough to offset the unit declines for many years, they aren’t any longer. In recent quarters, aggregate affiliate revenues have started to decline too.

There is little reason to expect the pace of subscriber declines to moderate. In the past, many have theorized that the pay TV subscriber base will converge on the population of hardcore sports fans. But with it now almost inevitable that sports will move outside the bundle (made more stark by Disney’s recent acknowledgement that it’s working on offering a streaming version of core ESPN and the challenges in the RSN business), there is no longer a logical floor to the number of traditional pay TV subs.

Figure 3. Pay TV Sub Declines are Accelerating Too

Source: SVB MoffettNathanson

As mentioned, the other two components of video revenue are streaming and studio. Streaming has been an engine of revenue growth, but to a large degree at the expense of linear and, in any case, subscriber growth seems to be stalling out (notwithstanding the near-term benefit Netflix may be seeing from its recent decision to crack down on password sharing). Though less scrutinized, studio revenues have also been declining owing to reduced licensing to third parties, a shrinking home entertainment business and weakness at the box office.

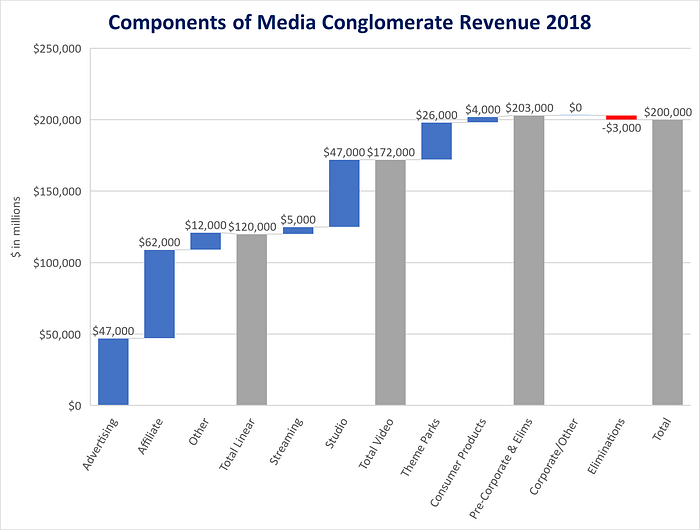

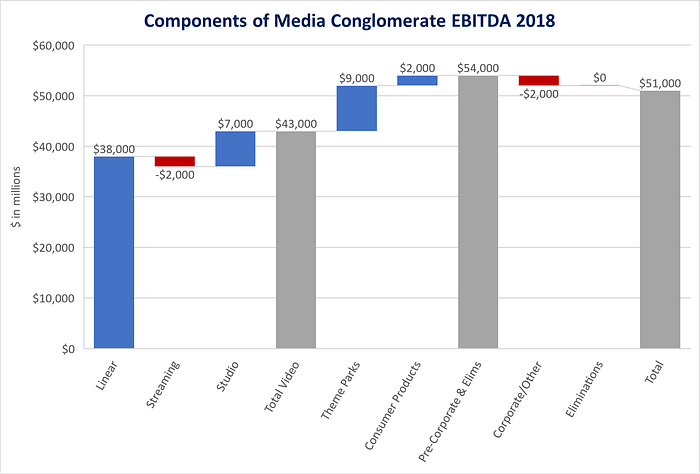

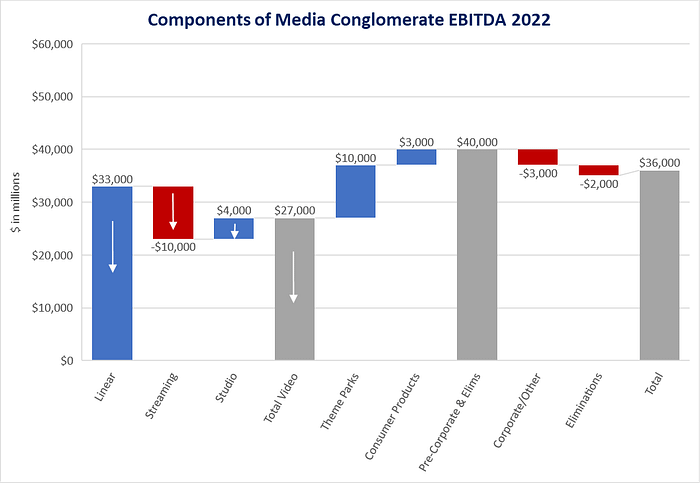

All of this can be seen in Figures 4 and 5. These compare the aggregate revenue and EBITDA for the media conglomerates in 2018 and 2022. I chose 2018 because it preceded the conglomerates’ big push into streaming (namely the launches of Disney+, Paramount+, discovery+ and HBO Max/Max).

The 2018 total includes CBS, Discovery, Disney, Fox, NBCUniversal, Viacom and WarnerMedia and the 2022 total includes all the same assets, now reconstituted into (a larger) Disney, (a much smaller) Fox, NBCUniversal, Paramount (the combination of CBS and Viacom) and WarnerBros. Discovery (the combination of Discovery and WarnerMedia).

There’s a lot going on here, but there are a few high-level takeaways:

- Linear revenue and EBITDA have declined over the period. Part of this is due to the dynamics mentioned above, such as the pressure on linear advertising revenue, which I calculate has declined by ~10% over the period. It is also due to the reclassification of some linear revenues to streaming. For instance, WarnerBros. Discovery now counts all HBO affiliate revenue as streaming revenue, which alone accounts for the entire decline in affiliate revenue shown in Figure 4. Otherwise, it would’ve been closer to flat.

- Streaming revenue is substantially higher (by ~$30B), but losses have increased a lot (~$8B).

- Studio revenues and EBITDA are also down substantially.

- The net effect of all of this is that aggregate video revenues are up marginally (6% over four years), but video profits are down ~35% over the period.

Figure 4. Aggregate Video Revenue is Up Marginally Over the Past 4 Years

Figure 5. Aggregate Video Profits are Down by 1/3 Over the Same Period

Notes: Each category represents global revenue/EBITDA. Figures rounded to the nearest billion. 2018 is the aggregate results of CBS, Discovery, Disney, Fox, NBCUniversal, Viacom and WarnerMedia. 2022 is the same assets included in 2018, reconstituted into Disney (now including most of the former Fox assets), Fox, NBCUniversal, Paramount (the combination of CBS and Viacom) and WarnerBros. Discovery (the combination of Discovery and Warner Media). 2018 Disney results are pro forma the consolidation of Hulu for comparison purposes. Does not adjust for non-calendar fiscal years (Disney is September, Fox is June).

So, video revenue growth has stagnated, despite the big push into streaming, and profits are way down.

How easy would it be to reinvigorate video revenue growth?

Video Already Attracts a Lot of Time and Money

The only way the video business can grow revenue is if consumption grows or it increases the monetization per unit of consumption, but both will be tough. I wrote about this recently in Video’s Fundamental Problem: It Over-monetizes, so I’ll repeat a few charts I used in that post.

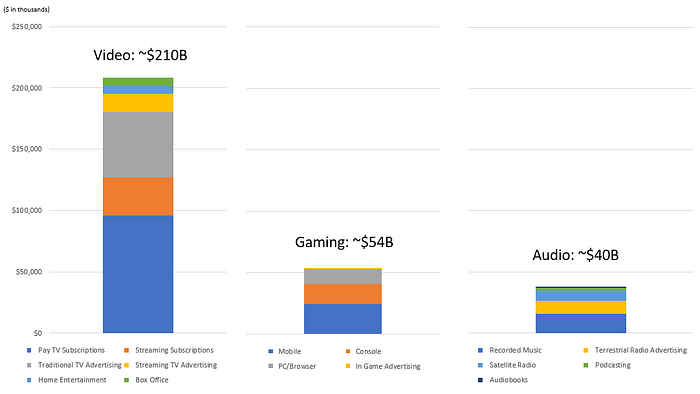

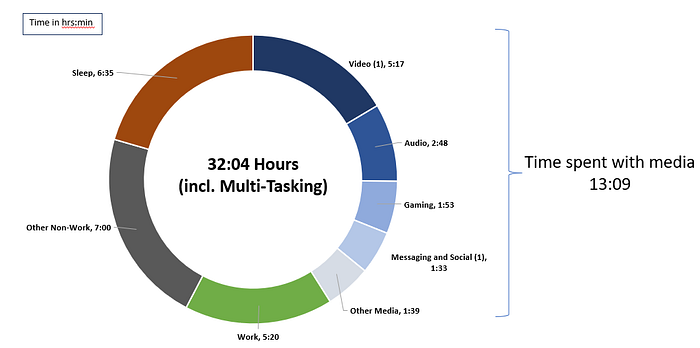

In Figure 6, I calculate that the size of the retail video market in the U.S. (pay TV, streaming, box office and home entertainment) was about $210 billion last year. (Note that this is not strictly comparable with the revenues of the media conglomerates shown above in Figures 4, since those are both wholesale and global.) That’s 4X the gaming market and 5X the audio market in the U.S. With about 130 million households in the U.S., it also equates to about $130 in monthly video spend per household.

In the U.S., the average household spends $130 monthly on video and the average adult spends more than 5 hours with video per day

Figure 6. In the U.S., the Retail Video Market Was 4X Gaming and 5X Audio Last Year

Source: Company reports, Morgan Stanley, Omdia, Box Office Mojo, Digital Entertainment Group, SensorTower, NPD Group, IFPI, RAB, eMarketer, IBISWorld, Author analysis

Looking at the market from the top down like this also provides a sense of the sheer magnitude of the challenge to growth. Let’s say that you assume the aggregate video business declines by 1% per annum (reflecting continued decline in linear and modest growth in streaming). Over five years, that’s $10 billion of end-market revenue (consumer spending and/or advertising) that must be replaced just to stay flat; 2% per year would create a $20 billion hole.

A 1% annual decline in end-market video revenue over five years would create a $10 billion hole; 2% would yield a $20 billion hole

The related issue is that video is also the largest recipient of consumer time spent with media. As shown (Figure 7), according to Activate, in 2021 the average U.S. adult spent over 5 hours per day watching long form video. This number can’t climb much from these levels. There are only so many hours in the day and a lot of other activities compete for consumers’ attention.

Figure 7. The Average U.S. Adult (18+) Watches 5+ Hours of Video per Day

Note: 1. “Video” excludes social video (YouTube, TikTok, etc.), which is included in “Messaging and Social.” Behaviors averaged over 7 days. Figures do not sum due to rounding. Sources: Activate analysis, Activate 2022 Consumer Technology & Media Research Study (n = 4,001), Company filings, Comscore, Conviva, Edison Research, eMarketer, Gallup, GWI, Interactive Advertising Bureau, Music Biz, National Sleep Foundation, Newzoo, Nielsen, NPD Group, Pew Research Center, U.S. Bureau of Labor Statistics, YouGov

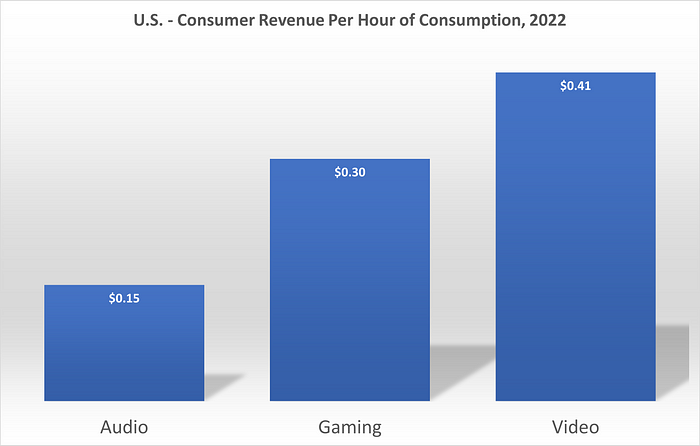

Video Arguably Over-Monetizes

Not only does video represent a lot of media money and time, but as I pointed out in Video’s Fundamental Problem, it arguably over-monetizes per unit of consumption, at least relative to other media. This can be calculated simply by dividing the total retail revenue (Figure 6) by the total time spent (Figure 7), to produce Figure 8. As shown, on a per-hour basis, video monetizes 50% more than gaming and 3X audio.

Figure 8. Video Monetizes at Almost 50% More Per Hour than Gaming and Almost 3X Audio

Source: Author analysis

Why is that? Here’s an except from Video’s Fundamental Problem:

[H]istorically people were paying too much money for too much video. That is a vestige of the “forced bundling” of the traditional pay TV bundle, in which people were paying a lot for a lot of networks they didn’t watch.

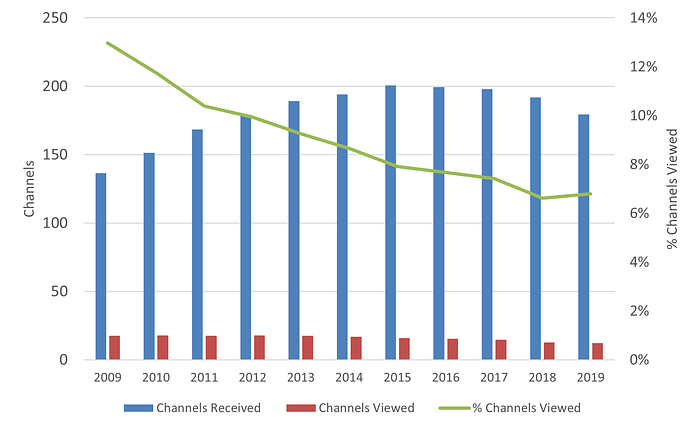

As shown in Figure 9, between 1995–2015, cable prices rose about twice as fast as inflation. Plus, according to Nielsen, the number of networks that consumers viewed monthly actually declined over that period (falling from ~17 to ~12), even as the number of networks they received continued to climb (Figure 10).

Figure 9. Cable Price Increases Substantially Outstripped Inflation…

Source: FCC Report on Cable Industry Prices, Oct 12, 2016 via Cordcutting.com

Figure 10. …And Subs Were Increasingly Paying for Channels They Didn’t Watch

Source: Nielsen

Streaming, by contrast, is effectively unbundling the bundle by enabling consumers to assemble their own synthetic bundle (Netflix, Hulu, Disney+, HBO Max, etc.). Since they are now better able to select the services they use, this is better aligning consumption with expenditure.

Remember, I’m shooting for pragmatic optimism here. That frames out the pragmatic part: media conglomerates are essentially video companies, video is (currently) in decline, it already attracts a lot of time and money and arguably has historically over-monetized relative to other forms of media.

Alright, let’s shift to the optimistic part.

Where Will Growth Come From?

Stepping back from the considerable challenges, the media conglomerates have a few things going for them:

- Some of their current problems are self-inflicted and therefore potentially reversible.

- They make a product that people spend enormous amounts of time consuming and love.

- They own or control vast amounts of intellectual property (IP).

- While Internet economics — such as plummeting distribution costs — are always deflationary and therefore value destructive for incumbents, they are accessible to incumbents too.

With this as a starting point, we can identify a few broad categories of potential growth:

- Fix it. They can reverse some of the profit pressures caused by the headlong rush into streaming. This is the lowest hanging fruit and is already well underway.

- Better monetize attention. While it is unlikely that they will persuade people to spend even more time with video, they can better monetize people’s attention, either directly or as top-of-funnel to something else.

- Better monetize engagement. Similarly, they can better monetize people’s “love” — or what is more commonly called engagement — by providing them new ways to interact with their content and IP.

- Capitalize on Internet economics. This includes expanding geographically and exploiting new lower-cost production technologies.

- Shrink-to-grow. They can divest their most challenged assets to focus on the best opportunities for growth.

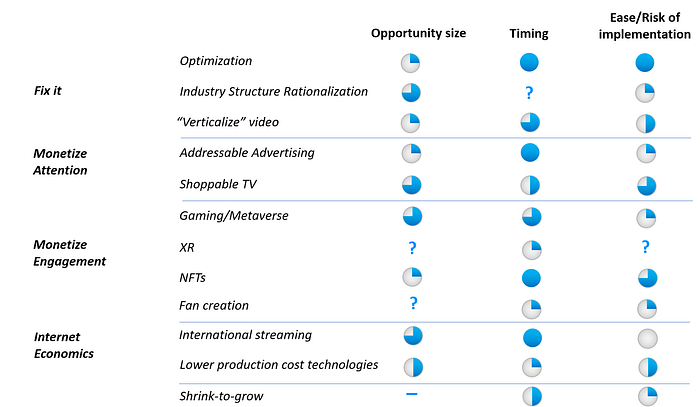

Below, I provide an overview of specific opportunities in each of these categories. Each of these probably warrant their own essay or, in some cases, already have.

None of the conglomerates have articulated a long-term growth strategy, but they need to

What jumps out clearly from this laundry list: there is no silver bullet and none of this will be easy. Some of these initiatives sound good on the surface but less so with a little digging. Some would require significant investment, which is probably not realistic in the current austere environment. Some are already in process, but others are much more speculative and will take a lot of time and many things to go right to develop. But beyond improving streaming profitability, none of the media conglomerates have articulated a long-term growth strategy. They need to. In totality, these initiatives should help.

Figure 11. A Summary of Potential Growth Initiatives

Source: Author

Fix It

As alluded to above and I have written about before (such as in One Clear Casualty of the Streaming Wars: Profit), pay TV was one of the great all-time businesses. At the peak, close to 90% of TV households subscribed and paid for a lot of TV networks they didn’t watch.

Then Netflix showed up. The conglomerates watched, mostly helplessly, and in many cases haplessly, as subscribers and viewers started to flee. Once most of the damage was done, they belatedly and reluctantly jumped into streaming, hoping they would obtain some of Netflix’s growth and multiple. They did, but it was short lived.

Put differently, Netflix dug a hole, the conglomerates jumped into the hole and then realized they are in a hole. The glory days of pay TV will never return. But there are ways to dig out.

Optimization

“Optimization” refers to the collective efforts of the industry to make operational changes that improve video profits (see Media’s Shift From Growth to Optimization).

This process is already well underway, with numerous steps geared to both boost revenue and profitability:

- Price increases (most recently aggressive price increases from Disney+)

- New ad tier offerings (Netflix and Disney+)

- Crackdown on password sharing (Netflix and Disney)

- Moderation in the pace of content spend across the board

- Content optimization, including embracing theatrical and more licensing of content to third parties (Disney, Paramount and WarnerBros. Discovery)

- More analytical approaches to subscriber management (e.g., more sophisticated measurement of marketing spend, personalized offerings, predictive churn management, etc.)

These efforts should help overall industry profitability and enable the conglomerates to staunch their streaming losses. But they are unlikely to yield much growth. Streaming has far low consumer switching costs than the traditional TV business, so price increases and reducing content spend, both of which degrade the consumer value proposition, may be pushing on a string because consumers can just churn faster.

Industry Structure Rationalization

A few months ago, I posted an essay called What Will Streaming Peace Look Like? that explores potential structural changes in TV. The premise was that while “optimization” may help, ultimately the market can’t support seven independent, vertically-integrated streaming services.

All of these services are replicating the same infrastructure costs and many don’t have enough compelling content, which reduces pricing power and increases churn. There are two ways to reduce the number of distinct, competing services: either through consolidation or “synthetically,” through bundling. (Or some combination of the two.)

The former would be more elegant. Consolidation of streaming services would enable elimination of duplicative costs, a larger content budget and library and, as a result, (presumably) better pricing power and lower churn. The chief problem is that the regulatory environment may not allow it. And, even if it could go through, is it worth the risk? Given the pressure in the business, a long period of uncertainty while negotiating regulatory approval may be untenable.

Without an accommodative regulatory environment, bundling is the next best option

A more compelling bundle of multiple services (with one app, universal search and recommendation, a clear bundled discount) wouldn’t carry all the same benefits as consolidation, but it could at least reduce churn and acquisition costs.

In recent months, the industry has taken a few baby steps in this direction. YouTube recently introduced Primetime Channels, a service that, similar to Amazon’s Prime Video Channels, aggregates up multiple streaming services. Disney announced intentions to bundle Hulu with Disney+ into one app to create a “more unified experience.” And at a recent investor conference, WarnerBros. CEO David Zaslav said that “[t]here should be a consolidation, but it is more likely to happen in the repackaging and marketing of products together.”

The “Verticalization” of Video

Credit for this idea goes to Rameez Tase, co-founder of analytics firm Antenna, in this post. In theory, this could fall under the “optimization” category above, but I thought it warranted its own call-out. The gist is that the conglomerates would benefit by combining FAST/AVOD, SVOD and, although Tase doesn’t write this, TVOD services into one unified experience.

In the good ol’ days of pay TV, the video experience was aggregated. You had all your broadcast and cable networks, free on demand content and transactional on demand content (or what used to be called pay-per-view) in one place: your cable set-top box. Today, all of that content is now disaggregated, both horizontally and vertically, among dozens of FAST/AVOD offerings (Pluto, tubi, Freevee, Roku Channel, etc.), SVOD (Netflix, Hulu, Disney+, Max, etc.) services and TVOD storefronts (such as on Amazon Prime or Apple iTunes).

As he points out, you can think of FAST/AVOD as top-of-funnel and SVOD as middle-of-funnel. Additional purchase opportunities like TVOD (or merchandise or anything else) would be bottom-of-funnel. In other words, the free, ad-supported services attract the most subscribers, some subset of those are persuaded to pay a monthly subscription fee for additional content and some subset of those are willing to make additional one-off purchases. The chief benefits of unifying these services into one app would be severalfold:

- It could attract new SVOD subscribers who enter the FAST/AVOD funnel.

- It could reduce re-acquisition costs. As mentioned above (and I’ve written about before in To Everything, Churn, Churn, Churn), churn is a big problem. There has been a lot of discussion about how to reduce churn, which in turn would improve LTV/CAC (lifetime value/customer acquisition cost) by increasing LTV. But an alternative approach is not to reduce churn, but to reduce CAC. If subscribers churn off the SVOD service but remain in the “ecosystem” by still watching FAST/AVOD content, it will be a lot less expensive and more efficient to retarget them.

- It could provide the most motivated fans the ability to purchase additional products.

Figure 12. Three FAST Channels Now Make the Cut

Source: Nielsen

As linear pay TV has declined, FAST/AVOD growth has exploded. Three FAST services, tubi, Pluto and Roku Channel, are now large enough to warrant inclusion in Nielsen’s monthly streaming report (Figure 12). But none of these are associated with an SVOD service. tubi is owned by Fox, which has no general entertainment SVOD; similarly, Roku has no SVOD service; and although Pluto and Paramount+ are both owned by Paramount, there is (somewhat inexplicably) no relationship between the two apps. Both Hulu and Peacock used to offer a free tier, but both have discontinued it. The closest to what I’m describing is Amazon, which embeds Freevee (FAST and AVOD), Prime Video SVOD, Prime Video Channels and Prime Video TVOD all into one experience.

Unifying FAST/AVOD, SVOD and even TVOD in one experience could boost subs and improve LTV/CAC

Better Monetize Attention

As mentioned before, people spend an almost unfathomable amount of time watching video. Could it be monetized better?

Addressable/Programmatic Advertising

TV viewership and advertising is transitioning from linear to streaming. On the surface, this seems like an opportunity for the conglomerates to better monetize ad inventory. In reality, there are a few reasons it is probably only a marginal benefit, if that.

Linear TV advertising is a broad reach vehicle. Historically, linear TV — like print, radio and outdoor — was a top-of-funnel medium. It was (and is) used by advertisers primarily to reach a lot of people, create awareness and drive intent. Ad inventory is sold mostly by a direct ad sales force and pricing for a TV ad unit is based on estimates of how many people watch, or “gross rating points” (GRPs). These estimates are provided by Nielsen, based on a panel of ~40,000 households. These GRPs are broken down by broad age and gender cohorts, such as Adults 18–34, Men 18–49, Kids 2–11, Women 25–54, etc. In other words, TV is a pretty blunt tool and it is high touch, so in the U.S. only about 10,000 of the largest advertisers tend to advertise on TV. The top 200 reportedly represent about 1/2 of the total.

TV is historically a blunt tool and high touch

For many broad-based marketers (like, say McDonald’s or Nike), they may be trying to reach as many humans as possible. Other marketers purchase specific age/gender cohorts as a proxy for their targeted customers, which invariably creates some inefficiency. For instance, let’s say that Chevrolet is targeting “light truck intenders” and launches a campaign paying an average $20 CPM for all men 18–49 delivered. If, in fact, only 33% of those men 18–49 are really its target, then it is effectively paying a $60 CPM to reach them.

For years, cable networks have attempted to improve the yield on their inventory by selling it more efficiently. These efforts have had some success, but they are hampered by significant drawbacks:

- Addressable linear. Networks have partnered with cable (and, more recently, satellite) operators to sell addressable linear advertising, which targets different ads to different households. These distributors know their customer base (unlike networks, which are wholesalers) and, using digital ad insertion (DAI) technology, they can send different ads to different households. However, it hasn’t moved the needle a ton. E-marketer estimates that linear addressable will be ~$4 billion this year in the U.S., about 6% of the TV ad market. One challenge is that almost all addressable advertising is delivered using the distributors’ local ad “avails,” generally only two minutes per hour. In addition, the friction to plan and execute addressable buys is high and measurement is difficult.

- Audience targeting. As another approach to improving the yield on linear inventory, all of the cable networks have also tried to offer new ad products that sell behavioral cohorts, or “audiences” (yogurt lovers, home design enthusiasts, etc.), rather than just an age/gender demo. Although these ads aren’t addressable, the premise is that they can improve efficiency through better media plans. Since they don’t know exactly who is watching their programming, these products are based on models that predict which cohorts will watch which programming. I haven’t seen estimates for the aggregate amount of ad revenue sold this way, but it is still an imprecise process and suffers from a lack of standardized measurement. OpenAP, a consortium of the largest network groups, is working to create common standards for targeting and measuring audiences across networks, but it’s a work in progress.

Streaming advertising offers several advantages over linear. Streaming, or CTV (“connected TV”), advertising holds the promise of dramatically increasing the feasibility of addressable advertising on TV. With the recent launches of both Netflix and Disney+ ad-supported plans, all the major streamers now offer ads. All CTV ad inventory is inherently addressable (i.e., different ads can be sent to different households) and CTV providers know information down to the household level (they usually have first-party data, such as credit card and email addresses, and can enrich this data with third-party data sets to build out a comprehensive view of customer attributes). This enables both better targeting and, to some degree, better measurement of ad efficacy. In addition, much of this inventory is sold programmatically (i.e., on an automated basis, through private or open markets), increasing the efficiency of the buying process. Unified ID 2.0 (UID2) is an open-source framework first developed by The Trade Desk to enable a unified identifier across CTV homes, which has now been adopted by every major CTV provider (other than Netflix). This enables marketers to better target and measure viewers across “publishers.”

CTV should be the holy grail for marketers. Is it as good for the conglomerates?

In theory, all of this is pretty good news for the streamers. CTV offers a combination of “brand safety” on TV, targeting and measurement. Owing to the greater efficiency, CTV inventory is usually priced at a premium to linear inventory on a CPM basis. Other than broadcast or cable primetime originals, linear inventory can go for $10–15 CPMs, while CTV CPMs can range from $25–65. Targeting should be more efficient, possibly enabling streamers to satisfy advertisers’ goals with less inventory and free some up to be sold elsewhere or used to satisfy “make goods” (the industry term for under-delivery of audience guarantees, which networks generally try to satisfy by providing more inventory, not refunds). In addition, programmatic buying is more accessible for a larger number of advertisers, especially mid- and long-tail businesses whose budgets aren’t large enough to warrant linear TV buys. While around 10,000 advertisers use TV, more than 10 million use Facebook.

In reality, the benefits for the conglomerates are probably marginal. There are a bunch of reasons for this:

- CTV budgets will probably come mostly from linear — so, for the conglomerates, it’s zero-sum. Ultimately, total TV advertising revenue is the aggregation of all TV advertising budgets. While ad budgets may shift between TV, digital and other media over long periods of time, these are all run by different teams with different goals and workflows. From a practical standpoint, advertisers do not view different media as fungible. So, growth in CTV on TV will likely come largely at the expense of linear TV. That may be a huge boon to Netflix and Amazon because they don’t have any linear networks, but it isn’t for the media conglomerates.

- A lot of streaming viewing isn’t ad supported. Since aggregate TV viewing is relatively flat, every lost minute of linear viewing shifts over to streaming, pretty much 1:1. However, a significant portion of streaming viewing isn’t ad supported. Netflix and Disney’s ad-supported offerings are relatively new and even for the streamers that have long offered both ad-free and ad-supported tiers, on average about 50% of customers still opt for ad-free (depending on the streamer).

- Streamers are competing against other CTV providers. In addition to the streamers, FAST/AVOD services that are unaffiliated with the conglomerates (Freevee and the Roku Channel) and connected device platforms (Roku, Vizio, Samsung) also offer CTV ads. For instance, Roku generally keeps about 30% of the inventory for ad-supported services distributed on its platform.

- Attracting the “long-tail” may not matter a lot. Most of the long-tail, smaller businesses that advertise primarily on digital are digital-native and their ad operations are geared to performance advertising. As they grow larger, they may have more interest in growing brand awareness and moving some of their marketing higher up the funnel. But for the most part these bottom-of-funnel marketers are trying to reach a specific consumer with a specific problem at a specific time — when they are ready to make a purchase. Unlike digital, TV doesn’t convert. The idea of “shoppable TV,” namely being able to complete a transaction on your TV, has been around a long time. It has never amounted to much. (More on this below.) Until TV makes it easy for consumers to complete a transaction, it won’t be as attractive to marketers trying to hyper-target. Unless…

Shoppable TV

Can TV become a full-funnel medium?

As mentioned above, the idea of shoppable TV, or what used to be called T-commerce, has been around a long time. Sometime in the mid 1990s — when TVs were supposed to be the endpoints of the “Information Superhighway” and Time Warner Cable was experimenting with interactive TV in Orlando — I told my girlfriend (now wife) that one day she would be able to click on Jennifer Aniston’s sweater, while watching Friends, see who made it and buy it. She likes to remind me how wrong I was about that. Today, the proportion of people who have ever purchased anything interactively on a TV (excluding calling a 1–800 number) probably rounds to zero.

You still can’t buy Jennifer Aniston’s sweater on your TV

Is shoppable TV a real opportunity or a chimera? There are a few reasons to be hopeful this time around. People have (obviously) overcome their reluctance to buy online and digital payments infrastructure is mature. (E-commerce is a massive market — according to Statista, ~$3 trillion globally in 2022.) The growth of live shopping and social commerce have shown consumers’ willingness to make purchases directly from video ads. Consumers have also long been willing to make purchases through TV, namely on HSN and QVC and on direct response “informercials.” Also, keep in mind that it is technically possible to sell items featured both in ads and in programming (shows and movies). And while TV is historically a top-of-funnel medium, it is the only top-of-funnel medium with a return path. Unlike newspapers, outdoor or radio, TV is interactive.

TV is the only top-of-funnel medium with an endemic return path

A few months ago, NBCU announced plans to offer shoppable TV on Peacock with its partner KERV Interactive as well as license the platform to third parties, expanding on prior tests. Initially, it requires viewers to scan a QR code on their phones to make a purchase, but the next step is to enable this with a remote.

Clearly, the more frictionless this can get, the better. Viewers should be able to easily add something to a cart and use an integrated wallet. The purchase process can’t interfere with the narrative of the show, so there needs to be a way to shop fast during commercial breaks, complete the transaction on a second screen as the video keeps playing or save it in a shopping cart to complete later. But the pieces are in place for what I think is an intriguing idea and one of the few large untapped pools of revenue that may be available to TV networks. Plus, as described above, one of the fringe benefits of turning TV into a full-funnel medium is that it could make addressable advertising more compelling to performance marketers.

The pieces are in place for what I think is an intriguing idea

Better Monetize Engagement

From IP as Platform:

According to a study by Troika, 85% of people say they are a fan of something, and 97% of people aged 18–24. Especially at a time when religious affiliation continues to decline, for a lot of these people, their fandom is a vital part of their identity. (That’s exemplified by the prevalence of brand tattoos.)

For many people, the object of their fandom is entertainment IP. Anyone who has been to ComicCon, E3 or a Harry Styles concert has seen that, as does anyone who has been on the wrong side of fan backlash.

While Disney is the clear exception, generally media conglomerates are not great at monetizing this devotion. If your fandom is, say, Game of Thrones, you currently have limited opportunity to engage. You can read the books, maybe re-watch everything other than the disappointing last season, perhaps see if there’s anything new on the Game of Thrones wiki, or even fly to Morocco or Dubrovnik to tour the sets and then what? In theory, there are many additional ways for the conglomerates to monetize their fans’ “love” than is generally occurring today.

Fair warning: other than gaming, all of what I cite below is pretty speculative.

Gaming/the “Metaverse”

Whether you think gaming is an attractive opportunity for the conglomerates depends on how you define it and your perception of their risk tolerance. More so than any other option I discuss in this essay, to really move the needle in gaming would require a very large, if not bet-the-company, commitment.

To establish a real presence in gaming would require a massive commitment

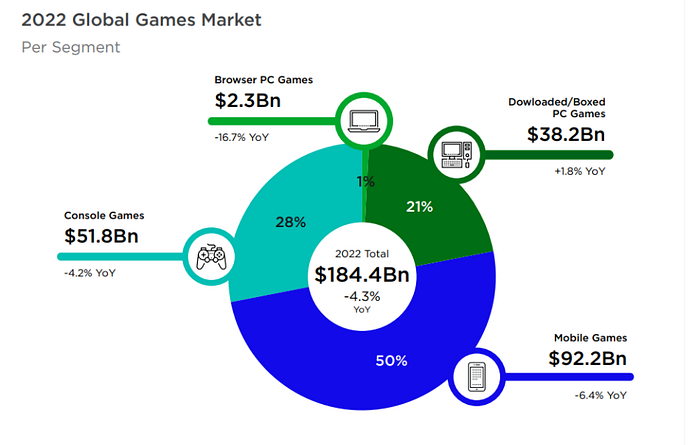

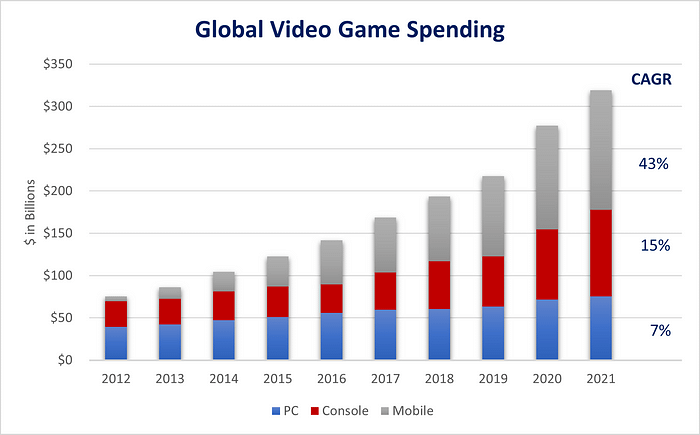

Globally, the gaming business represents a large revenue pool. According the NewZoo, it was ~$185 billion last year (Figure 13), compared to the roughly ~$450 billion in global end market video revenue. And, as shown in Figure 14, it is growing a lot faster than anything else that could be called “media.”

Figure 13. Gaming is a ~$185 billion Market

Source: NewZoo

Figure 14. Gaming is Growing Fast

Source: Morgan Stanley

Moreover, increasingly, games are not just games. They are social hubs, communication tools, live events venues, fashion shows and parallel economies. Dutifully and predictably hewing to the Gartner hype cycle, “metaverse” has recently become a derided word. But if you set aside the requirement that the metaverse be experienced through some sort of XR device and define it as a persistent digital environment in which participants are represented by an avatar, then it’s already in full swing at Roblox and Fortnite. It seems increasingly clear that the “metaverse” will evolve out of gaming.

It seems increasingly clear that the metaverse will evolve out of gaming

It is probably uncontroversial to claim that, for many fans, they would love to step into alternative realities based on their favorite IP — to wander around Diagon Alley, Westeros, Gotham, Tatooine or Wakanda. Having the capabilities to create these worlds would give the conglomerates multiple new and probably unanticipated ways to monetize their fans’ devotion.

Despite the promise of gaming, it’s hard to get too pumped up, for several reasons:

- The conglomerates have mostly tried and failed before. Today, Warner Bros. (Warner Bros. Interactive Entertainment) and Sony (Sony Interactive Entertainment) are the only filmed entertainment studios with a significant games presence. (Although, Sony doesn’t really count; it’s more so a games company with an entertainment presence than the reverse.) WBIE has been profitable in recent years, but not enough to really move the needle. In 2016, after years of effort and hundreds of millions in losses, Disney shuttered Disney Interactive Studios and moved to a licensing model. Universal and Paramount also license their IP.

- Hit TV and film adaptations into games are few and far between. Lately there have been a few good examples of successful translations of gaming IP into film and TV. These include The Super Mario Bros. Movie (currently the #1 movie of 2023 at the box office), The Last of Us on HBO, The Witcher and Arcane (based on League of Legends) on Netflix and Halo on Paramount+, with many more in the pipeline (Assassin’s Creed, God of War, Mass Effect, etc.). History suggests that it’s much harder to create a compelling interactive experience from linear storytelling than the reverse. Putting aside comic book IP, which isn’t really film IP, other than this year’s blockbuster Harry Potter Hogwarts Legacy and several Star Wars titles made under license by Electronic Arts (EA) (the Battlefront games, Jedi: Fallen Order and Jedi: Survivor), there have been only a few middling entries over decades of trying. The conglomerates own (or have a close relationship with the owners of) a vast amount of IP with rich mythology and rabid fan bases that, at least theoretically, could be translated into successful game franchises: Lord of the Rings, Game of Thrones, Minions, Star Trek, The Matrix, James Bond, Avatar, Alien, Indiana Jones, etc., etc. But all of these have been made into video games, in some cases several times, with little success.

- Gaming is extraordinarily competitive. It’s not like Activision, EA, Nintendo, Microsoft, Sony, Take Two and Ubisoft are just sitting around.

- Above all: to have a move-the-needle position in gaming would require a massive commitment. A serious effort in gaming would likely require significant M&A (such as buying one of the remaining big independent publishers, like EA, Epic or Take Two). Each game also entails a significant operational investment. A single AAA console title can easily top $100 million in development costs and gaming companies usually have multiple games in development simultaneously. Whether any of the conglomerates currently have the appetite for this kind of bet is unclear.

XR

By all accounts, the Apple Vision Pro is a monumental achievement that exceeds the performance of any XR headset in the market. Plus, it’s Apple, which has a long history of being late to a category (music players, smartphones, tablets) and yet completely defining it. And yes, the price point of $3,500 is inaccessible, but this will likely come down (or they will introduce lower-priced models) in time.

Does it mean anything for the media companies? Tough to say. In one scenario, it’s little more than a cool new way to watch movies. In another, it’s the catalyst for the “metaverse” we just discussed. A third possibility is that it becomes a new modality for consumption of entertainment in new ways, as Disney CEO Bob Iger showed off at the Apple WWDC in June — for which the conglomerates could charge a premium.

In the best case scenario, this wouldn’t only apply to newly-created content. NeRF (neural radiance field) technology enables the creation of 3D imagery from 2D images — raising the possibility that one day all existing films could be converted into 3D volumetric video. This would enable viewers to watch a movie or TV show from any angle, including within the action itself. Could the Vision Pro herald a new way to monetize library? Maybe.

NFTs

Back before crypto winter set in, I wrote an essay called Every Media Company Needs an NFT Strategy-Now. Looks like I was a little off about the “now” part. However, I still believe in the value and utility of digital property rights, enabled by NFTs. In addition, it’s something the conglomerates could do now.

For media companies, there are a lot of potential benefits, but I think these are the two biggest: 1) scarce digital collectibles would create another way to engage and monetize the biggest fans; and 2) because NFTs are saleable, they would provide fans a financial stake in their favorite IP, making them even more ardent evangelizers.

Fan Creation

Above, I referred to a recent essay called IP as Platform, which argued that there’s an opportunity for media companies to harness their fans’ creative energy.

As AI evolves, many creators will use new production tools to develop entirely new stories and formats, but many will also want to create content that expands on their favorite fictional worlds — such as the media conglomerates’ IP. If past is prelude, the conglomerates will try to tamp that down. In the essay, I argued that the more progressive approach would be to encourage and enable fan creation (albeit within the right legal and economic framework). The benefits could include deeper fan engagement, free marketing, the possibility of sourcing new storylines and talent and, if these stories are monetized, boost revenue.

Exploit Internet Economics

At the risk of being a little hand-wavy, by “Internet economics,” I mean the tendency of the Internet to reduce barriers to entry along various points in the value chain. As mentioned at the beginning, this is always deflationary and therefore value destructive for incumbents. But incumbents can also try to take advantage of lower costs. For the conglomerates, two such examples are international expansion and lower production costs. Unfortunately, the former is not nearly as easy as it sounds and institutional friction may restrict their ability to capitalize on the latter.

International Streaming

Again, to grow, the conglomerates need to target large untapped pools of revenue. One of the initial rationales for the push into streaming was the international TV opportunity. But, for the most part, it hasn’t panned out as hoped and probably won’t.

One of the initial rationales for the conglomerates’ push into streaming was the international opportunity, but it’s much easier said than done

The aggregate size of the international TV market is slightly larger than the U.S. TV market. According to Magna Global, the TV advertising market is roughly $100 billion outside the U.S. (vs. about $70 billion within it) and S&P Global Market Intelligence also pegs international pay TV subscription revenues at around $100 billion, about equivalent with the U.S.

Even though the total TV market is bigger internationally, the conglomerates currently generate less than 20% of their linear TV revenue outside the U.S. Above (Figure 4), I estimated that the media conglomerates generated about $110 billion in linear revenue last year. Of this, I estimate that less than $20 billion was international. (Most of the conglomerates’ cable network businesses are ~25–30% international, but keep in mind that this $110 billion includes ~$30 billion of purely domestic broadcast TV.) Historically, it has been difficult for the conglomerates to profitably launch and scale networks outside the U.S. Many international territories have only a few (or even one), dominant pay TV distributor. Streaming makes it feasible to disintermediate these dominant local distributors.

Figure 15. In 2018, ~59% of Netflix Content Amort Was International

Note: Netflix last disclosed this breakout between domestic and international in 2018. Source: Company reports.

The reality, however, is that it is very difficult to build streaming scale internationally. Markets are very competitive, with Netflix, Amazon Prime and multiple local streaming services in most markets. Besides the cost to staff and launch new markets, the requisite content spend is also out of reach for most of the conglomerates.

International audiences expect both high-quality foreign content and substantial amounts of locally-produced content. The last time Netflix disclosed the allocation of its content amortization between “Domestic Streaming” and “International Streaming” was in 2018. At that time, International represented ~59% of content amortization (see the bottom of Figure 15). That proportion has likely risen to 65% or more since then as the company has ramped up local content investments. With ~$18 billion of cash content spend last year, that equates to ~$12 billion internationally. This is more than most streamers’ global content budgets.

In the current environment of fiscal austerity, it is unrealistic that the media conglomerates will be able to invest to build scale internationally. If anything, the opposite is happening. The most notable example is Disney’s recent decision to explore strategic options for Star India, an important strategic foothold in the fifth largest economy in the world. On its recent 3Q 2023 earnings call, management also said it is evaluating exiting other international markets. A less prominent example is that HBO recently re-upped its output deal with Sky NZ, effectively preventing it from rolling out Max in New Zealand. It’s output deals with Sky (which is unaffiliated with Sky NZ) in the UK, Germany and Italy expire in 2024 and it seems likely they will renew those too, not reclaim those rights for a big Western European push.

Lower Production Cost Structure

As mentioned above, in recent months, I’ve been writing a lot about how new technologies, namely virtual production and, yes, AI, are set to lower the costs of high quality content creation. (See Forget TV, Here Comes Infinite TV and How Will the Disruption of Hollywood Play Out?). Even though falling entry barriers are never a good thing for incumbents, the bull case is that the studios will lean into these technologies and also lower their own production costs.

Let’s take virtual production first. According to Rob Bredow, Chief Creative Officer of Industrial Light and Magic, there is now evidence “on the ground” that virtual production (specifically, shooting on a “volume,” a soundstage of LED screens that synthetically creates the location) can produce shoot time savings of 30–50% relative to shooting on location.

What about AI? At this point, it’s very hard to predict the degree to which AI will also reduce production costs and it’s a sensitive topic because reducing production costs is usually a euphemism for “reduce the number of people needed.” However, it is already clear that AI is on a path to dramatically reduce VFX and other pre- and post- production costs. For instance, VFX and AI company MARZ (Monsters Aliens Robots and Zombies) offers a product called Vanity AI that applies “digital makeup” at a far lower cost and time requirement than doing this work frame-by-frame. Rotoscoping, compositing, 3D modeling, developing crowd scenes and a lot of other post production work seems poised to benefit. As another example, Flawless and Deepdub offer seamless dubbing into any language — in the actor’s voice — providing a much better outcome and much lower cost than traditional localization services. Conveniently ignoring the controversy, over time AI will also probably be useful in enhancing more creative components of the production process, including writing, acting and perhaps even using text/image/or video-to-video tools to auto-generate some scenes.

Whether the major studios will capitalize on these sorts of technologies depends on both their cultures and the complexity of the ecosystems in which they operate. Disney reportedly has formed a task force to explore the use of AI in filmmaking. On the other end of the spectrum, Discovery WarnerBros. recently dismantled its “volume” in Leavesden because it couldn’t persuade the talent to use it. And, as has been well publicized, AI is already a flashpoint in the current WGA and SAG-AFTRA strikes and these issues will likely only become more complex and contentious.

Shrink-to-Grow

By “shrink-to-grow,” I mean divesting assets that are declining. This is essentially the strategy articulated by Disney CEO Bob Iger in a recent CNBC interview, when he signaled willingness to divest Disney’s linear entertainment TV assets (ABC and the cable networks, like FX and Freeform) and seek a partner for ESPN.

My own experience is that shrink-to-grow has a lot of merit if you can pull it off, but it carries a lot of risk and operational complexity

On the surface, this may seem like no strategy at all and just throwing in the towel. But I think it has a lot of merit, if you pull it off. The chief benefits are that it frees up management time and attention and it enables the company to once again articulate a credible “growth story,” which, as I discussed above, is critically important.

My experience is that business units with flagging results suck up a disproportionate amount of management bandwidth. When I was at Time Warner, we spun out AOL and Time Inc., both of which were shrinking at the time. Doing so enabled us to both articulate — and focus on — our opportunities as a pure-play video content company. Putting troubled assets in the right hands (such as a highly-motivated private equity owner) also increases the likelihood that they will get the necessary time and attention.

But shrink-to-grow also carries significant risks. Divestitures come at a cost. They exact a toll on the organization and signaling you are a motivated seller is not usually the best way to maximize value. Even worse, if no one shows up with a viable bid, you are then stuck with a wounded asset. They can be very difficult to disentangle operationally, which is especially the case for the media conglomerates, who all have tightly-entwined linear and streaming businesses. To take Disney as an example, so far the prospect of divesting broadcast and cable networks raises more questions than it answers. Will the content on these networks still be licensed to Hulu? Will ABC and ESPN still jointly bid for sports rights (including the all-important upcoming NBA rights)? What about ad sales operations?

Another key question is whether there are really buyers for a lot of troubled linear TV assets? It will probably be a fruitful (or at least busy) few years if you are an M&A banker or at a media-focused PE shop.

It’s Time to Look Forward

In fairness, it’s been a disorienting couple of years for the big media companies. They are reeling from the accelerating pressure on their core linear business and the realization that the big bets they made on streaming will not pay off as hoped. It’s understandable that they are retrenching.

Nevertheless, they need to grow or at least articulate a credible plan to try. Other than promising to improve streaming profitability and make good content, none of them are articulating how they’ll do that. It’s time to figure it out.